Mastering the Basics of Accounting: The 3 Golden Rules of Debit & Credit

Basis of Accounting: The Three Golden Rules of Debit & Credit

If accounting feels confusing at first, that’s completely normal. Almost every beginner faces the same fundamental question:

❓ “What should I debit and what should I credit?”

The confusion doesn’t come from complexity—it comes from a lack of clear logic.

The solution lies in understanding the Three Golden Rules of Accounting. Once you stop memorizing and start applying them logically, accounting shifts from being confusing to becoming simple, structured, and intuitive.

Let’s learn this step-by-step with examples, visuals, and quick quizzes.

Step 1: Understand the Core Concept- Build the Foundation

Before rules, understand the accounting equation:

Assets = Liabilities + Capital

Every transaction impacts this equation. Debit and Credit are just tools to maintain this balance.

Step 2: Account Classification (Very Important)

Types of Accounts

- Personal Account

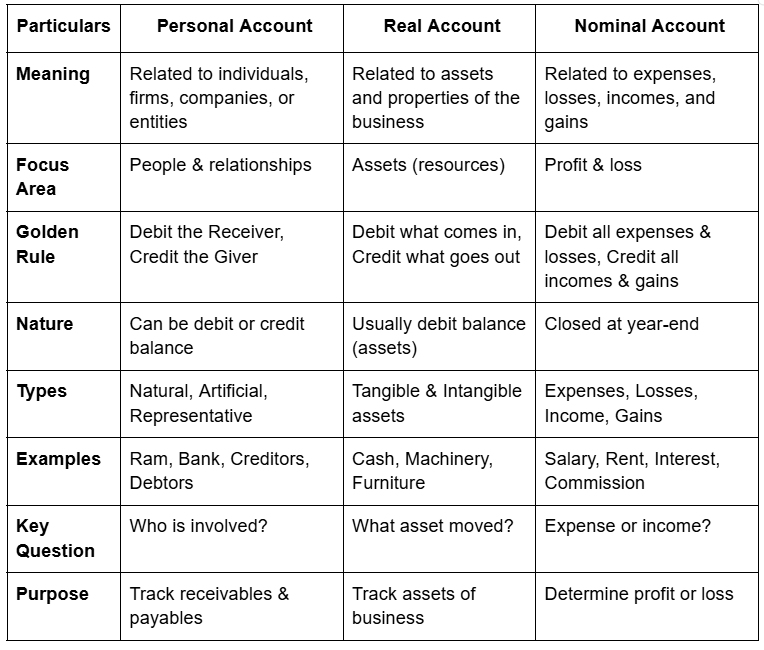

A Personal Account in accounting refers to accounts related to individuals, firms, companies, banks, or any organization, focusing on the relationship between the business and other parties. It follows the golden rule “Debit the Receiver, Credit the Giver,” meaning the person who receives value (cash, goods, or services) is debited, and the person who gives value is credited. Personal accounts are classified into Natural (real persons), Artificial (entities like companies or banks), and Representative (accounts representing a group, such as outstanding salary). The key to applying this concept correctly is identifying who is involved and who benefits in a transaction, rather than just looking at cash flow.

- Real Account

A Real Account in accounting relates to assets and properties of the business, including both tangible (cash, machinery, furniture) and intangible assets (goodwill, patents). It follows the golden rule “Debit what comes in, Credit what goes out,” meaning when an asset enters the business it is debited, and when it leaves the business it is credited. Real accounts focus on the movement of resources within the business, and they carry forward from year to year. The key to applying this rule correctly is identifying what asset is coming in or going out, rather than who is involved in the transaction.

- Nominal Account

A Nominal Account in accounting relates to expenses, losses, incomes, and gains of the business, such as salary, rent, interest, and commission. It follows the golden rule “Debit all expenses and losses, Credit all incomes and gains,” meaning any expense or loss incurred is debited, while any income or gain earned is credited. These accounts are used to determine the profit or loss of the business and are closed at the end of the accounting period. The key to applying this rule correctly is identifying whether the transaction represents an expense (outflow) or income (inflow) affecting profitability.

Comparison of Personal, Real & Nominal Accounts-

Instead of memorizing rules mechanically, focus on the underlying logic of each transaction:

- Who is involved? → Identify Personal Account

- What asset is moving? → Identify Real Account

- Does it impact profit or loss? → Identify Nominal Account

By training your mind to think this way, journal entries become logical rather than confusing, helping you achieve accuracy, clarity, and fewer errors in accounting.

Conclusion

The Three Golden Rules of Accounting are far more than just theoretical concepts—they are the foundation of every financial transaction recorded in practice. Whether you are working on journal entries, bookkeeping, financial reporting, or advanced ERP systems like SAP or QuickBooks, these rules guide every step of the process.

By applying these rules effectively, you can:

- Simplify journal entries by logically identifying what to debit and credit instead of memorizing

- Reduce errors by ensuring correct classification of accounts (Personal, Real, Nominal)

- Strengthen conceptual clarity, which is crucial for handling complex transactions like accruals, adjustments, and provisions

- Improve accuracy in financial statements, as every correct entry contributes to reliable reporting

- Enhance decision-making skills, since clean accounting data leads to better financial analysis

Most importantly, mastering these rules helps you move from:

Mechanical accounting (just posting entries)

to

Analytical accounting (understanding the flow of value)

This shift is what differentiates a beginner from a professional accountant.

Shweta Goyal, CA, CPA

CA | CPA (License Awaited) | Expert in U.S. Taxation, Accounting, Auditing, and Regulatory Compliance

Mastering the Basics of Accounting: The 3 Golden Rules of Debit & Credit

Basis of Accounting: The Three Golden Rules of Debit & Credit

If accounting feels confusing at first, that’s completely normal. Almost every beginner faces the same fundamental question:

❓ “What should I debit and what should I credit?”

The confusion doesn’t come from complexity—it comes from a lack of clear logic.

The solution lies in understanding the Three Golden Rules of Accounting. Once you stop memorizing and start applying them logically, accounting shifts from being confusing to becoming simple, structured, and intuitive.

Let’s learn this step-by-step with examples, visuals, and quick quizzes.

Step 1: Understand the Core Concept- Build the Foundation

Before rules, understand the accounting equation:

Assets = Liabilities + Capital

Every transaction impacts this equation. Debit and Credit are just tools to maintain this balance.

Step 2: Account Classification (Very Important)

Types of Accounts

- Personal Account

A Personal Account in accounting refers to accounts related to individuals, firms, companies, banks, or any organization, focusing on the relationship between the business and other parties. It follows the golden rule “Debit the Receiver, Credit the Giver,” meaning the person who receives value (cash, goods, or services) is debited, and the person who gives value is credited. Personal accounts are classified into Natural (real persons), Artificial (entities like companies or banks), and Representative (accounts representing a group, such as outstanding salary). The key to applying this concept correctly is identifying who is involved and who benefits in a transaction, rather than just looking at cash flow.

- Real Account

A Real Account in accounting relates to assets and properties of the business, including both tangible (cash, machinery, furniture) and intangible assets (goodwill, patents). It follows the golden rule “Debit what comes in, Credit what goes out,” meaning when an asset enters the business it is debited, and when it leaves the business it is credited. Real accounts focus on the movement of resources within the business, and they carry forward from year to year. The key to applying this rule correctly is identifying what asset is coming in or going out, rather than who is involved in the transaction.

- Nominal Account

A Nominal Account in accounting relates to expenses, losses, incomes, and gains of the business, such as salary, rent, interest, and commission. It follows the golden rule “Debit all expenses and losses, Credit all incomes and gains,” meaning any expense or loss incurred is debited, while any income or gain earned is credited. These accounts are used to determine the profit or loss of the business and are closed at the end of the accounting period. The key to applying this rule correctly is identifying whether the transaction represents an expense (outflow) or income (inflow) affecting profitability.

Comparison of Personal, Real & Nominal Accounts-

Instead of memorizing rules mechanically, focus on the underlying logic of each transaction:

- Who is involved? → Identify Personal Account

- What asset is moving? → Identify Real Account

- Does it impact profit or loss? → Identify Nominal Account

By training your mind to think this way, journal entries become logical rather than confusing, helping you achieve accuracy, clarity, and fewer errors in accounting.

Conclusion

The Three Golden Rules of Accounting are far more than just theoretical concepts—they are the foundation of every financial transaction recorded in practice. Whether you are working on journal entries, bookkeeping, financial reporting, or advanced ERP systems like SAP or QuickBooks, these rules guide every step of the process.

By applying these rules effectively, you can:

- Simplify journal entries by logically identifying what to debit and credit instead of memorizing

- Reduce errors by ensuring correct classification of accounts (Personal, Real, Nominal)

- Strengthen conceptual clarity, which is crucial for handling complex transactions like accruals, adjustments, and provisions

- Improve accuracy in financial statements, as every correct entry contributes to reliable reporting

- Enhance decision-making skills, since clean accounting data leads to better financial analysis

Most importantly, mastering these rules helps you move from:

Mechanical accounting (just posting entries)

to

Analytical accounting (understanding the flow of value)

This shift is what differentiates a beginner from a professional accountant.

Shweta Goyal, CA, CPA

CA | CPA (License Awaited) | Expert in U.S. Taxation, Accounting, Auditing, and Regulatory Compliance

Mastering the Basics of Accounting: The 3 Golden Rules of Debit & Credit

Basis of Accounting: The Three Golden Rules of Debit & Credit

If accounting feels confusing at first, that’s completely normal. Almost every beginner faces the same fundamental question:

❓ “What should I debit and what should I credit?”

The confusion doesn’t come from complexity—it comes from a lack of clear logic.

The solution lies in understanding the Three Golden Rules of Accounting. Once you stop memorizing and start applying them logically, accounting shifts from being confusing to becoming simple, structured, and intuitive.

Let’s learn this step-by-step with examples, visuals, and quick quizzes.

Step 1: Understand the Core Concept- Build the Foundation

Before rules, understand the accounting equation:

Assets = Liabilities + Capital

Every transaction impacts this equation. Debit and Credit are just tools to maintain this balance.

Step 2: Account Classification (Very Important)

Types of Accounts

- Personal Account

A Personal Account in accounting refers to accounts related to individuals, firms, companies, banks, or any organization, focusing on the relationship between the business and other parties. It follows the golden rule “Debit the Receiver, Credit the Giver,” meaning the person who receives value (cash, goods, or services) is debited, and the person who gives value is credited. Personal accounts are classified into Natural (real persons), Artificial (entities like companies or banks), and Representative (accounts representing a group, such as outstanding salary). The key to applying this concept correctly is identifying who is involved and who benefits in a transaction, rather than just looking at cash flow.

- Real Account

A Real Account in accounting relates to assets and properties of the business, including both tangible (cash, machinery, furniture) and intangible assets (goodwill, patents). It follows the golden rule “Debit what comes in, Credit what goes out,” meaning when an asset enters the business it is debited, and when it leaves the business it is credited. Real accounts focus on the movement of resources within the business, and they carry forward from year to year. The key to applying this rule correctly is identifying what asset is coming in or going out, rather than who is involved in the transaction.

- Nominal Account

A Nominal Account in accounting relates to expenses, losses, incomes, and gains of the business, such as salary, rent, interest, and commission. It follows the golden rule “Debit all expenses and losses, Credit all incomes and gains,” meaning any expense or loss incurred is debited, while any income or gain earned is credited. These accounts are used to determine the profit or loss of the business and are closed at the end of the accounting period. The key to applying this rule correctly is identifying whether the transaction represents an expense (outflow) or income (inflow) affecting profitability.

Comparison of Personal, Real & Nominal Accounts-

Instead of memorizing rules mechanically, focus on the underlying logic of each transaction:

- Who is involved? → Identify Personal Account

- What asset is moving? → Identify Real Account

- Does it impact profit or loss? → Identify Nominal Account

By training your mind to think this way, journal entries become logical rather than confusing, helping you achieve accuracy, clarity, and fewer errors in accounting.

Conclusion

The Three Golden Rules of Accounting are far more than just theoretical concepts—they are the foundation of every financial transaction recorded in practice. Whether you are working on journal entries, bookkeeping, financial reporting, or advanced ERP systems like SAP or QuickBooks, these rules guide every step of the process.

By applying these rules effectively, you can:

- Simplify journal entries by logically identifying what to debit and credit instead of memorizing

- Reduce errors by ensuring correct classification of accounts (Personal, Real, Nominal)

- Strengthen conceptual clarity, which is crucial for handling complex transactions like accruals, adjustments, and provisions

- Improve accuracy in financial statements, as every correct entry contributes to reliable reporting

- Enhance decision-making skills, since clean accounting data leads to better financial analysis

Most importantly, mastering these rules helps you move from:

Mechanical accounting (just posting entries)

to

Analytical accounting (understanding the flow of value)

This shift is what differentiates a beginner from a professional accountant.

Shweta Goyal, CA, CPA

CA | CPA (License Awaited) | Expert in U.S. Taxation, Accounting, Auditing, and Regulatory Compliance

Building the underlying operating system for the autonomous enterprise. Powering the next generation

of business leaders.

© 2026 PERSTOC.AI ALL RIGHTS RESERVED.